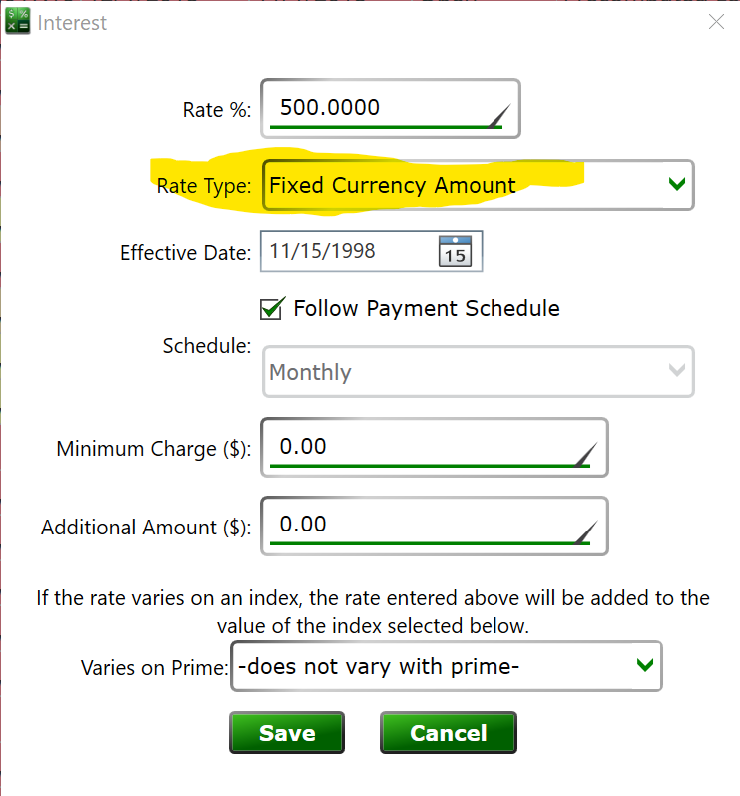

You’ve got a few ways you might tackle it. Probably the easiest – set the interest to a Fixed Currency Amount. If you know the monthly interest on $296,000 is, say, $500/month, you can set the interest rate to 500 and set the rate type to Fixed Currency Amount.

- mlp-fixed-currency-interest.png (83.27 KiB) Viewed 187653 times

Whenever interest is due, Moneylender will ignore the balance on the loan and just add the specified amount as interest. That’s the easiest, although you lose the ability to calculate per-diem interest.

Someone in a similar situation used the escrow account on the loan to track the credit available. Set up the loan for the full amount, and put an adjustment of $32000 to the Escrow account at loan origination. Then, as you disburse principal, instead of recording principal disbursements, you can record escrow adjustments (using negative numbers) to take the funds from the escrow account. Using adjustments, you’ll still see the transactions on the settings tab, just in the adjustment section. You can click “Escrow Account” to see their available credit balance. Meanwhile, the interest is accumulating on the full loan amount, and you still get per-diem interest on the loan at payoff and if the initial period isn’t exactly one month.

A third option is to set up the loan for the initial disbursal only, and then when you fund the remainder, record the principal disbursal to the date of origination. You might put the actual date disbursed in the description field. Depending on how you handle your books, having a retroactive principal disbursal might cause a headache. When the additional funds are disbursed on the origination date, Moneylender will recalculate the loan from inception, so you’ll end up with interest on the whole amount right from the beginning. If you edit the Loan Settings after creating the loan, you can set the Credit Limit to the full amount, and Moneylender can tell you the available credit (how much principal is still scheduled to be disbursed) as you disburse out that last $32k.

Depending on how you think the loan will go, these are three ways that handle it, each with their own strengths. The Escrow account option is probably the most robust.